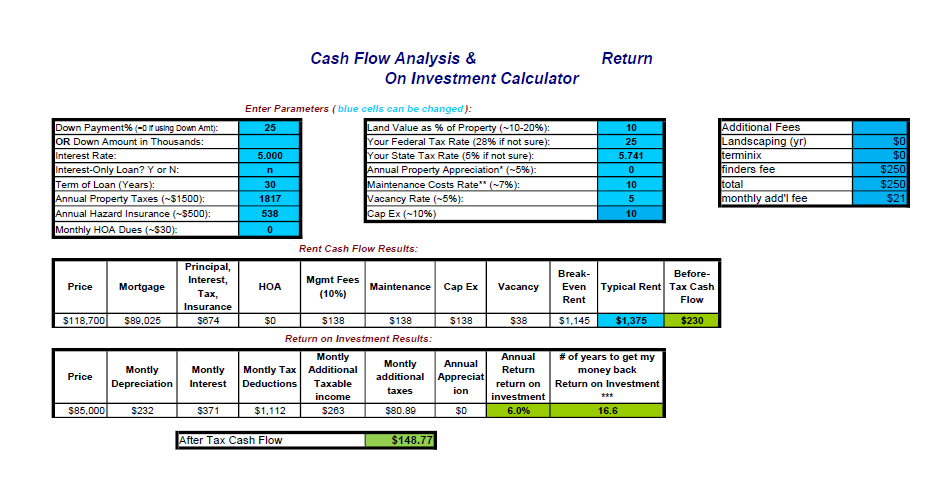

Should you buy stock or piece of real estate expecting it to go up in price?

Warrant Buffet once said, “Buy into a company because you want to own it, not because you want the stock to go up.” Or as I’ve also heard it said, never buy a piece of real estate or stock because you expect it to go up in price. Let me give you a practical example of breaking this rule and what I learned from it.

It’s 2003. I just got stationed in beautiful Phoenix Arizona. I attended a free presentation given by Robert Kiyosaki at the base theater. I was hooked. I quickly read Rich Dad, Poor Dad and everything else of his I could get my hands on. I highly recommend all of his books. The housing market in Phoenix starts to accelerate. Everyone’s making money on the appreciation of houses. Mortgage lenders are swamped because everyone is buying houses. They keep talking about the flood of people from the Midwest moving to the Southwest. I have friends who’s kids move out to Phoenix from Michigan, buy a house, and sell it six months later and make $60,000. The guys I’m hanging around with are talking about interest only loans and never paying them off. Being from the Midwest, that made no sense to me, but nonetheless I’ve read all of these books I can do this.

In early 2004 I buy my first investment property near where I live in Phoenix. I’ve got my team all lined up, a great realtor, a property management company, and a mortgage broker. As a side note, a great realtor is vital to real estate investing and do you want to know why? They know EVERYONE! If you need a plumber…call your realtor. If you need a new property manager…call your realtor. It’s a nice house with an HOA and everything. The market is Booming! I’m going to be rich. Well, with financing being so easy and everyone buying houses, why would anyone rent? It takes six months for me to get a renter. Realize I’m paying the mortgage, the hoa fees, everything. Once I do get a renter, I have negative $700 cashflow a month. No big deal right? The market is going straight up. About halfway through the year I realize, this is dumb. What if the housing market doesn’t keep going straight up? Why am I going to keep this investment and pay $700 out of my own money per month to keep it going. At the end of the year-long lease, I removed the renters and sell the property. Fortunately, I was single at the time with extra cash. I did sell the property for more than I bought it for, but with the negative cashflow and six months without rent, I’m lucky if I broke even.

That’s why you’ve heard me say, I never buy a piece of real estate expecting it to go up in value. I always assume the price will stay flat, or maybe even go down. Do I still want to hold the property? Does it still provide enough cashflow to be worth it to me? Hopefully you can learn from my mistakes and not make the same mistake yourself. “Only a fool learns from his own mistakes. The wise man learns from the mistakes of others.”

― Otto von Bismarck